Scapia credit card, known for its unlimited lounges and zero forex markup, has been one of the most talked-about lifetime free travel cards in India.

Is it actually worth the hype?

I added Scapia to my 20+ credit card stack six months ago. Here’s an honest, experience-based answer.

⚡️ Quick Verdict: Scapia is the easiest first travel card to recommend in 2026.

Lifetime free, unlimited lounge access, zero forex, and 2% base return on all eligible spends, and free airport perks every time you fly.

Card Overview

| Feature | Details |

|---|---|

| Issuer | Federal Bank / BOBCARD |

| Network | Visa + RuPay |

| Annual Fee | Lifetime Free |

| Forex Markup | Zero |

| Reward Rate | Up to 4% |

| Eligibility* | 750+ credit score; Income over ₹40k/month |

| Min. Age | 21 (salaried); 25 (self-employed) |

| Best For | Zero forex & unlimited lounges |

👆 Claim ₹1000 Flight Voucher ✈️

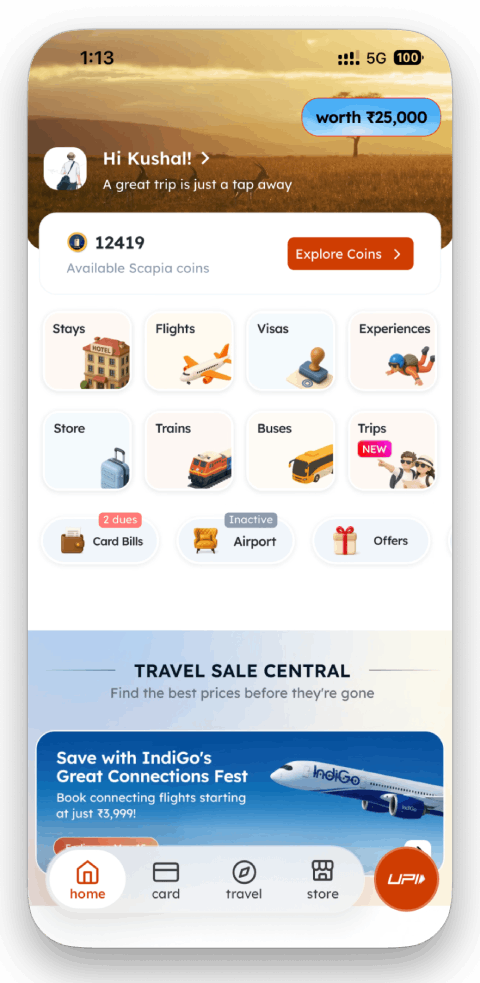

Rewards (Scapia Coins)

Every eligible spend earns 5 to 20 Scapia Coins — credited automatically on your statement date.

| Spend Type | Reward Rate | Effective Value |

|---|---|---|

| Eligible Visa spends | 10 coins per ₹100 | 2% |

| Scapia app spends | 20 coins per ₹100 | 4% |

| UPI spends (over ₹500) | 5 coins per ₹100 | 1% |

| International Spends | None (0% Forex) | – |

No earning cap — high spenders benefit proportionally. Plus, Scapia often runs travel sales boosting return up to 10%.

Excluded categories: Fuel, rent, wallet loads, insurance, utilities, EMI, cash, education, gift cards, govt., and international spends.

💡 I primarily use Scapia for offline swiping and jewelry shopping — both earn the full 2% with no capping.

Redeeming Scapia Coins

5 Scapia Coins = ₹1

| Redemption Option | Value |

|---|---|

| Flights, hotels, buses, trains (Scapia app) | 5 coins = ₹1 |

| Merchandise (Scapia Shop) | 5 coins = ₹1 |

| Statement credit | Not available |

| Redemption fee | ₹0 |

You can redeem up to 100% coins for your travel bookings — no partial redemption forced. That’s rare even on premium cards.

I redeemed coins for an Ambrane 10,000 mAh power bank via the Scapia Shop — price matched Amazon exactly.

Note: Coins are locked to the Scapia ecosystem. If you want flexibility beyond travel, pairing Scapia with the SBI Cashback Card ensures you’re covered for non-travel redemptions.

Lounge Access

Scapia offers unlimited domestic airport lounge access — rare for a lifetime free card.

| Airport | Lounge Access | Condition |

|---|---|---|

| Domestic | Unlimited | Spend ₹20K in prev. month |

| International | None | – |

Spend ₹20,000 in the previous month (combined across Visa and RuPay) and unlock lounge access for the entire next month — no visit cap, no per-quarter limit.

How it works:

- Open the Scapia app before your flight

- Toggle to lounge access

- Generate a QR code

- Scan at the lounge entrance

Best of all, add-on cardholders are eligible for lounge access too. They need to individually meet the ₹20,000 monthly spend on their own card.

💡 Tip: I use other premium cards for lounge access — no spend and keep Scapia for free airport dining or shopping — that way I’m getting value from both without wasting the airport privilege on lounge access.

HDFC Regalia Gold

Mid-range premium travel card with 5X rewards and flight vouchers.

- 12 Domestic & 6 International Lounge Visits per year

- ₹1,500 Nykaa/Myntra voucher on ₹1.5 Lakhs spend

- 5 Reward Points per ₹200 spent on retail

Airport Privileges

Each departure, the Scapia app lets you pick one benefit from four options:

- Free airport dining

- Free airport shopping

- Free airport spa

- Unlimited domestic lounge access

For example, on a typical domestic flight, you can either get up to ₹1,000 back on dining/shopping or choose unlimited lounges for that departure.

How it works:

- Select your option in the app before you fly

- Activate the outlet

- Pay with your Scapia card

- You get 100% back as coins on that spend

Earning Cap

| Terminal | Coins Back | Condition |

|---|---|---|

| Domestic | Up to ₹1,000 | ₹20K spend in previous month |

| International | Up to ₹2,000 | Book intl. flight worth ₹50,000+ via Scapia app in one transaction |

One benefit per departure. No annual cap on number of trips.

💡 Tip: Buy an Amazon Pay voucher if you’re short of the 20K milestone, it acts like currency. You won’t earn coins for gift card purchase but it counts for the spend milestone.

App Experience

The Scapia app is the best card management app I’ve used across 20+ credit cards I hold.

Why Scapia app stands out:

- Virtual card in ~3 hours of approval

- Check & activate lounge access within app

- Spend tracker

- Coin balance and redemption — everything in one place.

The interface is clean, fast, and doesn’t feel like a bank app. Most credit card apps bury features — Scapia surfaces what you actually need before a trip.

Additionally, add-on cardholders get their own app login with direct OTPs and individual transaction visibility — not a shared view.

Federal vs BOBCARD Scapia

Two versions of the Scapia card exist — same branding, different issuers.

| Parameter | Federal Bank | BOBCARD |

|---|---|---|

| Networks | Visa + RuPay combo | Visa + RuPay combo |

| UPI Payments | Yes (via RuPay) | Yes (via RuPay) |

| Reward & Benefits | Same | Same |

| Existing customer restriction | Existing cardholders can apply** | Same applies for BOBCARD |

| Availability | Widely available | Limited |

Key difference: Serviceability. Both cards, Federal and BOBCARD Scapia share the same benefits and rewards.

Which one to choose? You don’t get to choose — Scapia’s internal system decides the issuing bank based on your profile, location, and serviceability. Most new applicants I’ve seen still receive the Federal variant unless their area is exclusively serviced by BOBCARD.

My Application Experience

I applied directly through the Scapia app — the process is fully digital, no branch visit required.

- Application submitted and video KYC done within 10 minutes

- Virtual card issued in ~3 hours of approval

- Physical card arrived within 5 working days

The video KYC is straightforward — a short call where an agent verifies your PAN and address. Once that’s done, approval is fast.

Note: The approval process appears to be largely automated — no human review involved. Which also means rejections can happen for reasons Scapia won’t explicitly tell you. I’ve covered these in detail — 7 Real Scapia Rejection Reasons Nobody Will Tell You.

Referral Program

Scapia keeps surprising me with the best referral programs among lifetime free cards.

For instance, the current referral program lets you earn a Apple Watch SE 3 or ₹25,000 Amazon or Flipkart Gift Card.

Note: Scapia changes referral offers periodically — check the current offer before applying.

How to join

- Activate your virtual card

- Start referring Scapia to your friends.

Don’t have Scapia? Use my referral link and get a ₹1,000 flight voucher at no extra cost.

🔒 Safe & Secure via Scapia App

Card Design

You get two physical cards — Visa and RuPay.

The Visa card is punchy orange with a dark top panel.

The RuPay card is bright green with a pixelated QR pattern fading into the background — unmistakably Scapia.

Both feature matte finish and the same illustrated traveller — a figure walking with luggage — which fits the travel theme well. The cards feel premium in hand for a lifetime free product.

Note: The RuPay physical card isn’t issued automatically — I had to request it separately after receiving the Visa card.

Honest Pros & Cons

Pros:

- Lifetime free travel card

- 2% base return on all eligible spends — no upper cap

- Zero forex markup

- Free unlimited domestic airport lounge access

- Free airport benefits—dining / shopping / spa / lounge access— every time you fly

- Best-in-class app experience

- Fast digital application and virtual card

Cons:

- Coins are locked to the Scapia ecosystem

- No statement credit redemption

- No international lounge access

Mobodaily Rating

| Parameter | Rating |

|---|---|

| Rewards | 4.5 / 5 |

| Lounge Access | 4.5 / 5 |

| Fee Value | 5.0 / 5 |

| Zero Forex | 5.0 / 5 |

| App Experience | 5.0 / 5 |

| Customer Service | 4.0 / 5 |

| Eligibility | 4.5 / 5 |

Overall Rating: ⭐ 4.6/5, making Scapia card one of the best among free travel credit cards.

Final Verdict

After 6 months, the Scapia card remains in my wallet.

The only major requirement is a ₹20,000 monthly spend. Meeting this unlocks unlimited domestic lounge access, free airport dining or shopping, zero forex on international purchases, and a 2% return on eligible offline spends—all with no annual fee.

Its app is top-tier for a lifetime free card, offering honest pricing and simple redemption.

Scapia is my top recommendation for a first travel card in 2026. Certainly best for add-on card holders too.

Note: If this review helped you, applying via my link supports Mobodaily at no extra cost.

👆 Avail ₹1000 flight voucher 🎁

FAQs

Are the benefits the same on BOBCARD Scapia and Federal Bank Scapia?

Yes — rewards, lounge access, airport privileges, and zero forex are identical on both. The only practical difference is that BOBCARD’s RuPay card may not be issued automatically, requiring a follow-up with support.

Does Scapia really charge zero forex?

Yes. There is no forex markup on international transactions — what you spend abroad is exactly what gets charged. However, Scapia Coins are not earned on international spends.

Do I earn Scapia Coins on international transactions?

No. International spends are excluded from coin earning. You save on forex, but don’t earn rewards on those transactions.

Is Scapia still worth it after the 2026 devaluation?

Yes — zero forex, unlimited lounges, and airport privileges are all intact. What changed: the monthly spend threshold doubled from ₹10,000 to ₹20,000, and rewards on insurance and utilities were removed. For regular spenders, the value proposition still holds.

What are the best Scapia alternatives?

Depends on what you need. For higher rewards and international lounge access, AU Ixigo is the closest LTF alternative. For direct cashback, the SBI Cashback Card is a better fit. A full comparison is covered here —Best Scapia Alternatives.

How do I hit the ₹20,000 monthly milestone on Scapia?

The spend is combined across your Visa and RuPay cards. Most everyday spends count toward the milestone — including fuel (you get the surcharge waiver but no coins on it). Use the Scapia app’s spend tracker to monitor progress. If you’re short before a trip, buy an Amazon Pay voucher via the app to bridge the gap.

Disclaimer: This post contains my personal experience using the Scapia Federal Credit Card. Some links in this post are referral links — if you apply through them, I may receive a referral benefit at no extra cost to you. All opinions are my own and based on 5 months of actual usage. Credit card benefits are subject to change — verify current terms on the Scapia app or Federal Bank website before applying. You can read complete privacy policy and disclaimer here.

- Axis Horizon Credit Card Review: Worth ₹3,540 Fee? - July 29, 2026

- HDFC Marriott Bonvoy Credit Card Review (2026) - July 29, 2026

- HDFC Tata Neu Infinity Credit Card Review 2026 - July 24, 2026