Axis Atlas is gone. Horizon is what you get now — but is it any good?

5000 welcome edge miles easily justify the first year fee.

But Is the ₹3,540 fee justified second year onwards? Are the EDGE Miles transfer partners still worth chasing after Accor removal?

Holding the card for last six month in my 20+ credit cards, I’ll give you my honest review on Axis Horizon.

Overview

| Feature | Details |

|---|---|

| Card Type | Mid-premium travel |

| Network | Visa Signature or Mastercard World |

| Annual Fee | ₹3,000 + GST (₹3,540) |

| Welcome Benefit | 5,000 EDGE Miles |

| Reward Rate | Up to 5% |

| Lounge Access | 8 domestic/quarter 2 intl./quarter |

| Forex Markup | 3.5% + GST |

| Best For | Lounge Access & Moderate Travel |

Eligibility

The Axis Horizon is a mid-premium travel card, so the bar to get it directly isn’t low. While Axis Bank doesn’t officially publish a minimum income requirement for this card, based on community estimates, it typically expects:

| Parameter | Estimated Minimum |

|---|---|

| Credit Score | 750+ helps |

| Salaried | ₹50,000/month (₹6 lakh+ annually) |

| Self-employed | ₹8–10 lakh+ annual ITR |

| Age | 18–70 years |

Get 5,000 Edge Miles ✈️

If you meet the min requirements, apply via the above link.

But if you don’t — here’s the route I took.

How I got this card

I got the Horizon as a pre-approved upgrade offer on Axis My Zone card. No fresh application, no documents, no hard inquiry.

The strategy is simple:

- Apply for Axis My Zone (lifetime free, easy approval)

- Use it regularly and pay on time for 3 months

- Check the “Upgrade Offers” section in your Axis Bank app

That’s it. Axis quietly surfaces pre-approved upgrade offers once they see responsible usage — and the Horizon tends to show up for cardholders with a decent spend history.

👆 Lifetime Free | 1 yr SonyLiv | 1+1 on Movie Tickets 🍿

Fees & Welcome Benefit

| Parameter | Details |

|---|---|

| Joining Fee | ₹3,000 + GST (₹3,540) |

| Welcome Benefit | 5,000 EDGE Miles |

| Renewal Fee | ₹3,000 + GST (₹3,540) |

| Renewal Benefit | 1,500 EDGE Miles |

| Fee Waiver | None |

Is the ₹3,000 fee worth it?

Year 1 is effectively free — if you use the miles well. The 5,000 EDGE Miles welcome benefit is worth approximately ₹5,000+ when transferred to airline partners at a 1:1 ratio. So the joining fee essentially pays for itself.

Year 2 onwards you only get 1,500 renewal miles — worth roughly ₹1,500. That means you’re paying a net ₹2,000+ for the card annually unless you’re actively flying and redeeming miles at good value.

Welcome Benefit Credit

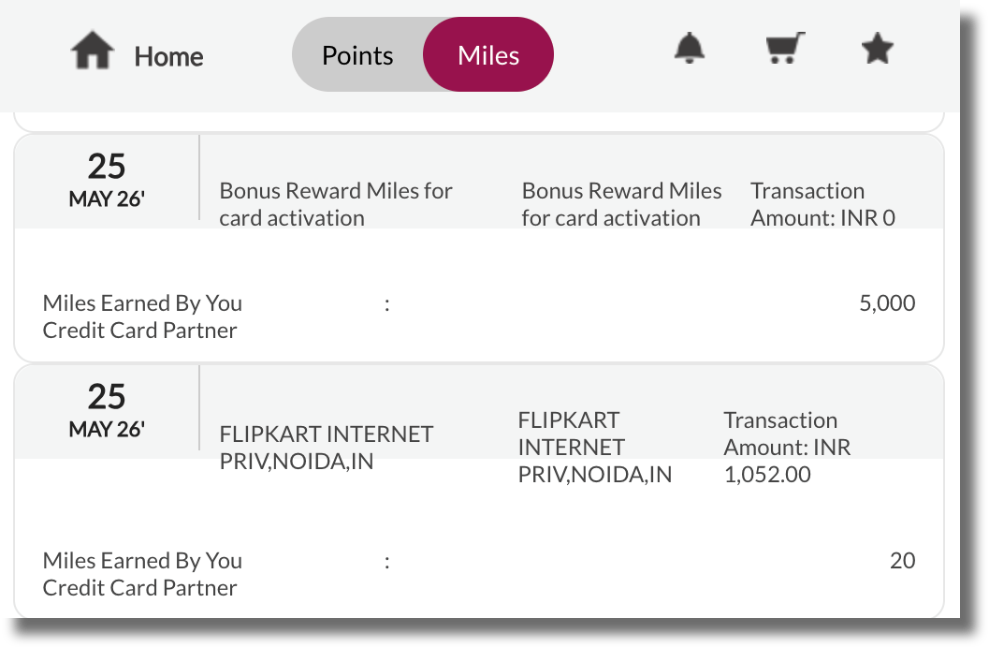

Welcome benefit of 5000 Edge miles got credited within 4-5 days after my first transaction.

⚠️ First Transaction Trap

Your first transaction (alone) must be ₹1,000 or more within 30 days of card issuance.

If first transaction is less than ₹1000, it will disqualify you from the welcome benefit entirely.

Rewards Structure

The Horizon keeps it simple. You earn EDGE Miles directly — no points-to-miles conversion, no confusing ratios.

| Spend Category | Earn Rate |

|---|---|

| Direct airline spends + Axis Travel EDGE portal | 5 EDGE Miles / ₹100 |

| All other retail spends (online + offline) | 2 EDGE Miles / ₹100 |

| Fuel, rent, utilities, insurance, govt, education, tolls, wallet loads | 0 EDGE Miles |

The 5x rate on hotels only applies when you book through the Axis Travel EDGE portal. Swipe directly at a hotel counter — even a Marriott or an ITC — and you earn just 2x. Always book hotels through the portal if rewards matter to you.

No milestone benefits. Unlike the Axis Atlas, the Horizon has zero milestone bonuses. Spend ₹1 lakh or ₹10 lakh — your earn rate stays flat. There’s no spend target to unlock better rewards, and no way to waive the annual fee through spending.

💡 Jewellery buyers take note: Unlike many premium cards, the Axis Horizon earns 2 EDGE Miles/₹100 on gold and jewellery purchases — it’s not in the excluded category. If you’re making a big jewellery purchase, swiping the Horizon is a smart move. A ₹1 lakh jewellery purchase = 2,000 EDGE Miles = ₹2,000+ in airline miles.

Reward Redemption

1 EDGE Mile = ₹1 when redeemed directly on the Axis Travel EDGE portal for flights, hotels, or experiences. That’s the floor — not the ceiling.

The real value comes from transferring to loyalty partners.

Transfer partners

The Axis Horizon credit card’s most significant benefit is its access to the same transfer partner network as the bank’s super-premium cards like the Magnus and Reserve.

Redemption Ratio: 1 EDGE Mile = 1 Partner Point / Air Mile

List of current transfer partners (as of May 2026):

| Group A (1L miles/year cap) | Group B (4L miles/year cap) |

|---|---|

| Aeroplan | Air Asia |

| The British Airways Club | Flying Blue |

| Ethiopian Airlines | Air India (Maharaja Club) |

| Etihad Guest | IHG One Rewards |

| Finnair Plus | ITC Hotels |

| JAL Mileage Bank | Orchid Rewards |

| Singapore Airlines KrisFlyer | The Postcard Sunshine Club |

| Royal Orchid Plus | Qantas Frequent Flyer |

| Turkish Airlines | Radisson Rewards |

| United MileagePlus | SpiceJet |

| Lotusmiles (Vietnam Airlines) | |

| Wyndham Rewards |

Edge Miles devaluation

On April 2, 2026, Axis silently removed Accor ALL, Marriott Bonvoy, and Qatar Avios from its partner list — zero notice to cardholders.

The obvious workaround — routing EDGE Miles via ITC Hotels into Marriott Bonvoy — was then shut down within weeks. ITC slashed its transfer cap from 10,000 to 5,000 points per quarter. The easy hotel redemption game is over.

Best way to transfer miles

Shift to airlines ✈️ — that’s the clear community consensus post-devaluation.

Air India Maharaja Club (Group B) is now the standout pick. It sits in Group B, so it doesn’t eat into your premium Group A quota. Axis periodically runs a 1:2 bonus transfer — every 500 EDGE Miles can become 1000 Flying Returns — the highest value redemption available right now on this card.

Singapore Airlines KrisFlyer (Group A) remains strong for international business class redemptions to Southeast Asia, Japan, and Europe. Best value for aspirational travel.

Flying Blue (Group B) runs monthly promo awards at discounted redemption rates — time your transfers around these for outsized value on Europe routes.

Avoid: Statement credit or cashback redemptions. Value drops well below ₹1/mile — you’re destroying the miles you earned.

Transfer cap

| Card | Group A cap | Group B cap | Total |

|---|---|---|---|

| Axis Horizon | 1,00,000 | 4,00,000 | 5,00,000 |

| Axis Atlas | 30,000 | 1,20,000 | 1,50,000 |

| Magnus / Reserve | 1,00,000 | 4,00,000 | 5,00,000 |

The Horizon matches Magnus and Reserve on transfer caps — and allows 3x more transfers than the Atlas. For a ₹3,000 fee card, that’s a genuinely underappreciated advantage.

Lounge Access

No spend conditions. Swipe your card at the lounge. Walk in.

| Parameter | Domestic | International |

|---|---|---|

| Visits per quarter | 8 | 2 |

| Access via | Visa Lounge Programme | Priority Pass |

| Add-on cardholders | Not Included | Not Included |

| Spend condition | None | None |

💡 Key Takeaway: Super-premium cards like the Axis Magnus (₹12,500/year) have ₹50,000 spend condition to unlock domestic lounge access. The Horizon at ₹3,000 has no such condition. Check out the list of 12 best cards for lounge access in 2026 – no spend.

Forex

The Horizon carries a 3.5% + GST forex markup — effectively ~4.13% on every international transaction. Any rewards earned abroad are largely negated by this fee.

For international travel, pair it with a zero forex card like Scapia or BOB Eterna for payments — use the Horizon only for the lounge access.

Axis Horizon vs Axis Atlas

| Parameter | Axis Horizon | Axis Atlas |

|---|---|---|

| Application Status | ✅ Active | ❌ Closed (since Aug 31, 2025) |

| Joining/Annual Fee | ₹3,000 + GST | ₹5,000 + GST |

| Spend-Based Fee Waiver | ❌ Not available | ❌ Not available |

| Welcome Benefit | 5,000 EDGE Miles on first txn of ₹1,000+ within 30 days | 2,500 EDGE Miles on first txn within 37 days |

| Renewal Benefit | 1,500 EDGE Miles on card anniversary | Tier-based: up to 5,000 EDGE Miles |

| Rewards – Accelerated | 5 EDGE Miles/₹100 on Travel EDGE & airline sites (uncapped) | 5 EDGE Miles/₹100 on travel spends (capped at ₹2L/month) |

| Rewards – Base | 2 EDGE Miles/₹100 on all other spends | 2 EDGE Miles/₹100 on all other spends |

| Points Transfer Ratio | 1 EDGE Mile = 1 Partner Point | 1 EDGE Mile = 2 Partner Points |

| Annual Transfer Cap | 5,00,000 EDGE Miles/year | 1,50,000 EDGE Miles/year |

| Excluded Categories | Fuel, Utilities, Insurance, Rent, Wallet, Govt., Education, Tolls/Transport | Fuel, Utilities, Insurance, Rent, Wallet, Govt., Gold |

| Forex Markup | 3.5% + GST | 3.5% + GST |

| International Lounges | 2/quarter (8/year) | Silver: 4 |

| Domestic Lounges | Visa: 8/quarter (32/year); Mastercard: 6/quarter (24/year) | Silver: 8 |

| Eligibility (Income) | ~₹6L net annual income | ~₹9L net annual income |

| Age | 18–70 years | 18–70 years |

My take: Horizon vs Atlas

Atlas excels in point value due to its 1:2 conversion ratio, doubling purchasing power for premium tickets. For travel spends of ₹1–2L monthly, its miles offer superior value compared to Horizon.

Horizon excels in flexibility and accessibility, being currently available for application. It features a lower ₹3,000 fee, uncapped accelerated earnings, superior domestic lounge access (32 visits/year), and a higher 5,00,000 annual mile transfer cap.

👉 Bottom line: Retain Atlas if you have it for the irreplaceable 1:2 ratio. For new applicants, Horizon is a strong, standalone travel card, particularly for domestic travel and frequent lounge use.

Axis Horizon vs HSBC TravelOne

| Parameter | Axis Horizon | HSBC TravelOne |

|---|---|---|

| Joining/Annual Fee | ₹3,000 + GST | ₹4,999 + GST |

| Fee Waiver | None | Spend ₹8 lakh/year |

| Welcome Benefit | 5,000 EDGE Miles on ₹1,000 spend within 30 days | 1,000 cashback + ₹3000 postcard hotel voucher |

| Reward Rate | 5 EDGE Miles/₹100 (airlines + Travel EDGE) · 2 EDGE Miles/₹100 (others) | 4 pts/₹100 (flights, travel portals, forex) · 2 pts/₹100 (others) |

| Excluded Categories | Fuel, rent, utilities, insurance, govt, education, tolls, wallets | Fuel, rent, utilities, insurance, govt, education, wallets |

| Forex Markup | 3.5% + GST | 3.5% + GST (effectively free till June 2026) |

| Transfer Partners | 19 partners · 1:1 ratio (most) | 20 partners · 1:1 ratio (most) · Accor + Marriott still active ✅ |

| Domestic Lounge | 8/quarter (32/year) · No spend condition | 6/year · No spend condition |

| International Lounge | 2/quarter (8/year) via Priority Pass | 4/year via LoungeKey |

| Airport Transfers | ❌ None | ✅ 4 complimentary/year (Toyota Hycross) |

| Eligibility | 750+ score · ₹6L+ salaried · Available PAN India | 750+ score · Salaried · Select cities only |

| Best For | Domestic frequent flyers wanting maximum lounge visits + Air India miles | International travellers wanting Accor/Marriott hotel points + airport transfers |

My take: Horizon vs T1

Pick TravelOne if you spend over ₹1 lakh per month on travel. Plus, Accor and Marriott are still active transfer partners on TravelOne while Axis removed them in April 2026. The 4 complimentary airport transfers are also a genuine differentiator no other card in this fee bracket offers.

Pick Horizon if you spend ~₹50K per month or fly domestically 2–3 times a month. 32 domestic visits a year (without spend conditions) at ₹3,000 fee is hard to beat.

👉 Key Takeaway: Horizon is for everyone including self-employed. TravelOne is for high travel spenders.

Honest Pros & Cons

Pros

- Strong Lounge Access—8 domestic lounges per quarter + 2 international per quarter via Priority Pass is repeatedly called the best mid-tier option.

- Solid First-Year Value from Welcome Bonus—5,000 EDGE Miles on ₹1,000 first spend (≥ ₹7,000 value transferred to partners) makes it a “no-brainer” for many.

- Practical Mid-Tier / Middle-Class Travel Card— a “good card” alongside stronger cards like Regalia Gold.

- Easy Accessibility + Renewal Perks—Lower eligibility barrier than Magnus and Regalia. Renewal still gives 1,500 EDGE Miles — enough for some users to justify keeping it as a secondary travel card.

Cons

- Sudden Devaluation Killed Travel Value—The April 2, 2026 removal of Accor, Marriott Bonvoy, and Qatar Airways is the #1 complaint.

- Welcome Benefit (5,000 EDGE Miles) Condition—You receive the welcome benefit when your first transaction is ₹1000 or more. Most users misunderstand the condition and fail to receive the welcome benefit.

- No lounge access for add-on card holder—Even users who like the lounge access (8 domestic/quarter) see this as a major drawback.

Mobodaily Rating

| Category | Rating |

|---|---|

| Rewards Earning | 4.0 / 5 |

| Lounge Access | 5.0 / 5 |

| Welcome Benefit | 5.0 / 5 |

| Transfer Partners | 3.0 / 5 |

| Forex & International Use | 2.0 / 5 |

| Fee Value | 4.0 / 5 |

| Customer Service | 4.0 / 5 |

| Overall Rating | 3.86 / 5 |

Should you apply?

Yes — Apply if:

- You are a frequent domestic traveler who can maximise up to 32 lounge visits/year on the Visa variant.

- You want easy first-year ROI (₹3,540 fee easily beaten by welcome miles + lounges).

- You are a multi-card holder looking to add a cost-effective Axis EDGE Miles earning card to your wallet.

- You already have an Axis relationship (higher approval odds).

No / Skip if:

- You travel internationally often — the 3.5% forex markup will eat into any rewards earned abroad

- You already hold Axis Atlas — its 1:2 EDGE Mile conversion ratio delivers far superior points value.

👆 Get 5,000 Edge Miles as welcome benefit 🎁

FAQs

Is Axis Horizon Credit Card worth it after the April 2026 devaluation?

It depends on your priority. It remains a strong choice for lounge access (up to 32 domestic + 8 international visits/year with no spend requirement). The official transfer ratio remains 1:1. However, the removal of Accor, Marriott, and Qatar Airways has reduced its long-term travel hacking value. Good for first-year ROI and lounges; not ideal for heavy reward chasers.

What is the welcome benefit and when is it credited?

You get 5,000 EDGE Miles on your first transaction of ₹1,000 or more within 30 days of card issuance. It is usually credited within 30–45 days, but many users report delays. If not credited, escalate via Nodal Officer or RBI Ombudsman (successful in several cases).

How do I register for Priority Pass lounge access?

Download the Priority Pass app or visit their website, create an account, and link your Axis Horizon card (it shows eligibility). You’ll get a digital membership. Some users needed to contact Axis support for confirmation. International access is limited to 2 visits per quarter.

Where can I transfer EDGE Miles now?

Current partners include Air India, British Airways, Finnair, Singapore KrisFlyer, Etihad, IHG, ITC, etc. Majority of transfers are at the official 1:1 ratio. Accor, Marriott Bonvoy, and Qatar Airways were removed on April 2, 2026.

What are the joining and annual fees? Can they be waived or refunded?

The official policy states “Fee Waiver: None”. Joining fee: ₹3,000 + GST (≈ ₹3,540). Annual/renewal fee: same.

You can request a waiver/refund within 45–60 days (especially post-devaluation), but success is not guaranteed. Email Nodal Officer or escalate if denied.

Does the card give lounge access to add-on cards?

No, domestic lounge access is available for primary card holder only (subject to quarterly limits). International Priority Pass usually works for primary cardholders; confirm with Axis for add-ons.

How good is the reward rate?

2 EDGE Miles per ₹100 on most spends; 5 EDGE Miles per ₹100 on Axis Travel EDGE and selected travel. Effective value dropped after devaluation (roughly 1–2% on regular spends without strong redemptions).

What are the charges for card replacement or block?

As of May 2026, Axis do not charge any card replacement fee for lost, stolen, or damaged card.

Should I close the card?

Many users closed it shortly after devaluation. If you value lounges and got good first-year use, keep it. Otherwise, transfer points first, then close via email (works better than calls) to avoid losing miles.

How is Axis customer service for Horizon card?

Mixed to poor. Welcome bonus delays, cancellations, and escalations are common complaints. Many users recommend emailing Nodal/Principal Nodal Officer or going to RBI Ombudsman for faster resolution.

Disclaimer: This post contains affiliate links. Views are personal and for informational purposes only — not financial advice. We advise you check the updated bank policy before making any financial decision. Read our full privacy policy and disclaimer.

- Axis Horizon Credit Card Review: Worth ₹3,540 Fee? - July 29, 2026

- HDFC Marriott Bonvoy Credit Card Review (2026) - July 29, 2026

- HDFC Tata Neu Infinity Credit Card Review 2026 - July 24, 2026