After using Scapia for 5 months, I must say it’s the best free travel card to get right now.

But the Scapia’s automated internal risk system is brutal. Many applicants with good income and credit profile got rejected.

No matter if you have 750+ CIBIL score, zero defaults, and a stable income, your application can still be rejected.

To identify the real Scapia rejection reasons, I analyzed hundreds of credit card forums and grievance team responses.

Let’s find out why your application failed and how to fix it.

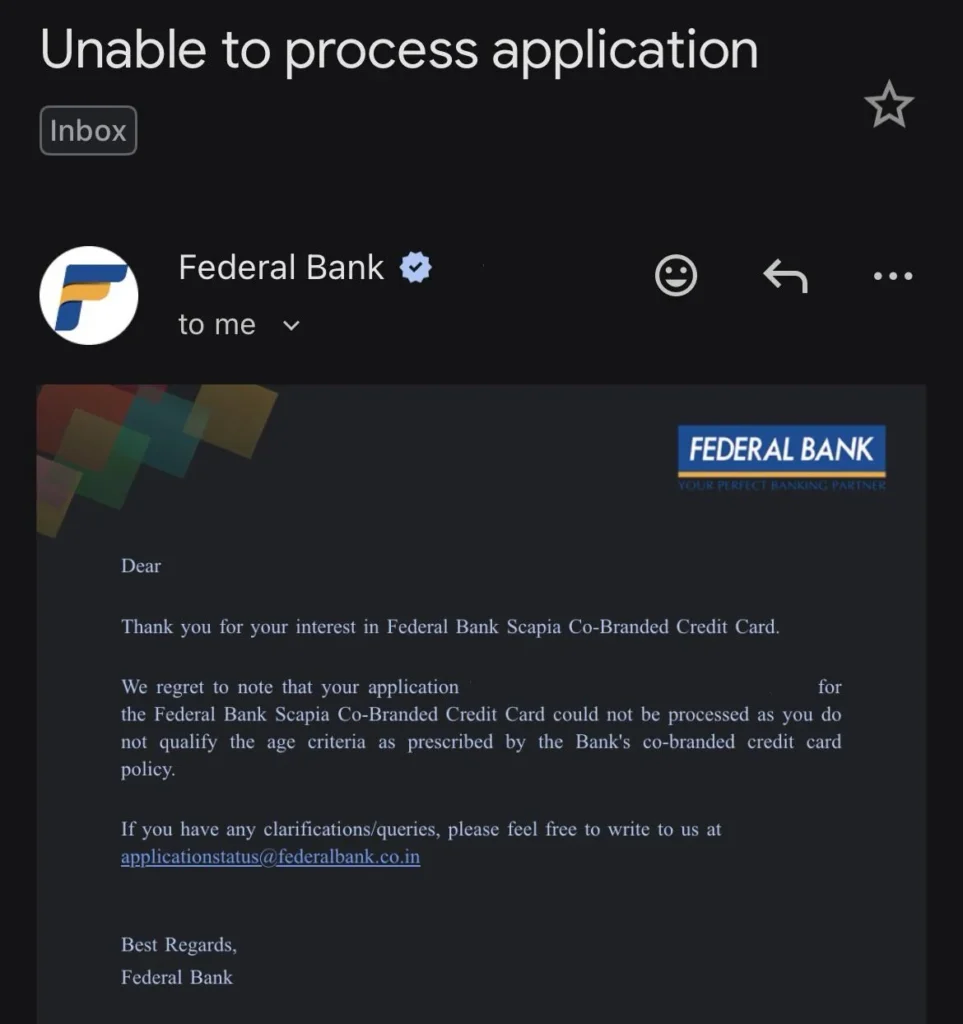

Vague Rejection Emails

When you hit ‘Submit’ on the Scapia app, their automated risk engine takes just seconds to evaluate your financial profile. If the system flags your application, you don’t get a detailed explanation from a human—you get a generic, automated template.

If you are reading this, there is a high chance you received one of these two confusing emails:

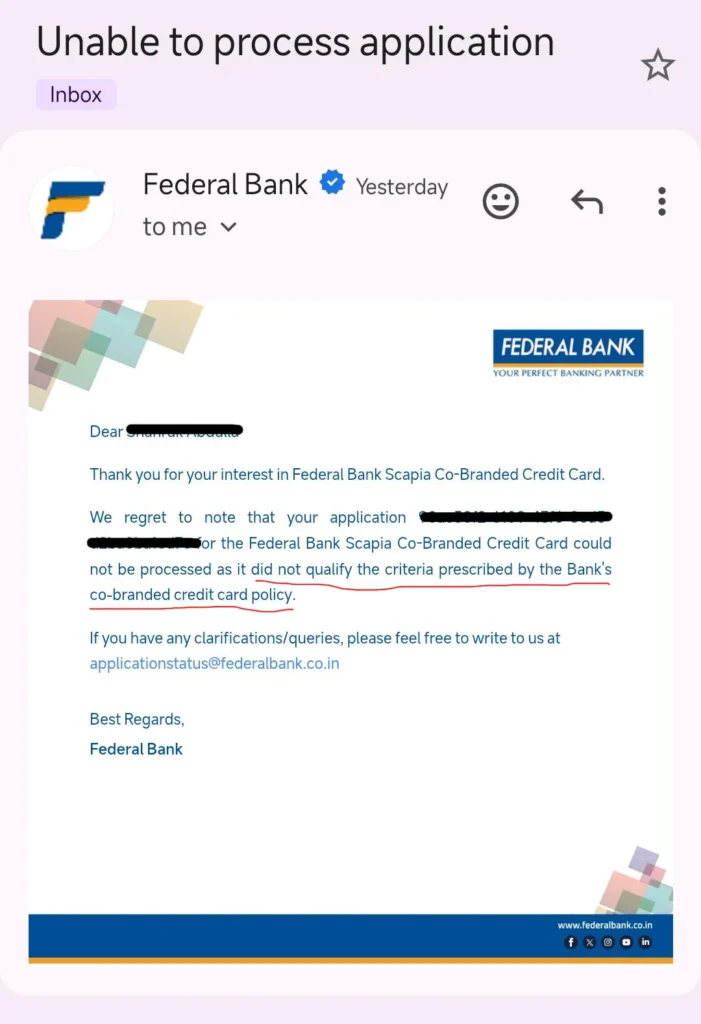

Not qualifying bank’s policy

This is by far the most frequent and frustrating email applicants receive. The message usually states that your details do not meet their internal policy or eligibility thresholds.

You check your CIBIL, see a pristine 780+ score with zero late payments, and wonder what went wrong.

The bank makes it sound like your credit history is flawed. In reality, this is a “catch-all” template used for hidden internal triggers.

As we will explore below, this email usually means you hit a hard wall like the “5-enquiry limit” or you already hold a Federal Bank credit card.

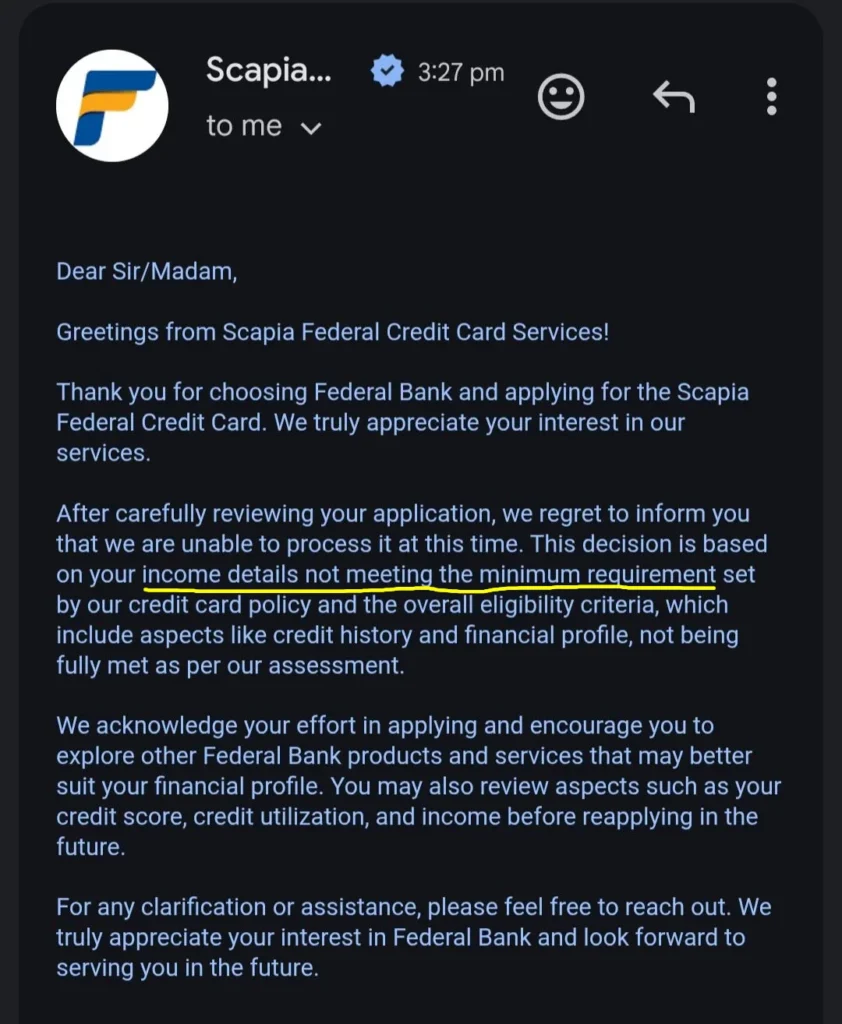

Income below requirement

Imagine earning over ₹1 Lakh per month, running a successful business, and receiving an email that claims your income is too low or doesn’t meet the eligibility criteria.

It feels like a system glitch, right? But it isn’t.

Scapia’s automated risk engine frequently uses this “income” excuse as a convenient cover-up when your profile fails any factor within their complex internal scoring system. The algorithm might actually be flagging you for a specific demographic rule (like the 25-year age limit for self-employed individuals), a short credit history, or even an unserviceable pin code.

Instead of simply telling you that you don’t meet the specific age or location requirement, the system defaults to the vague reasoning of your “overall income and eligibility criteria.”

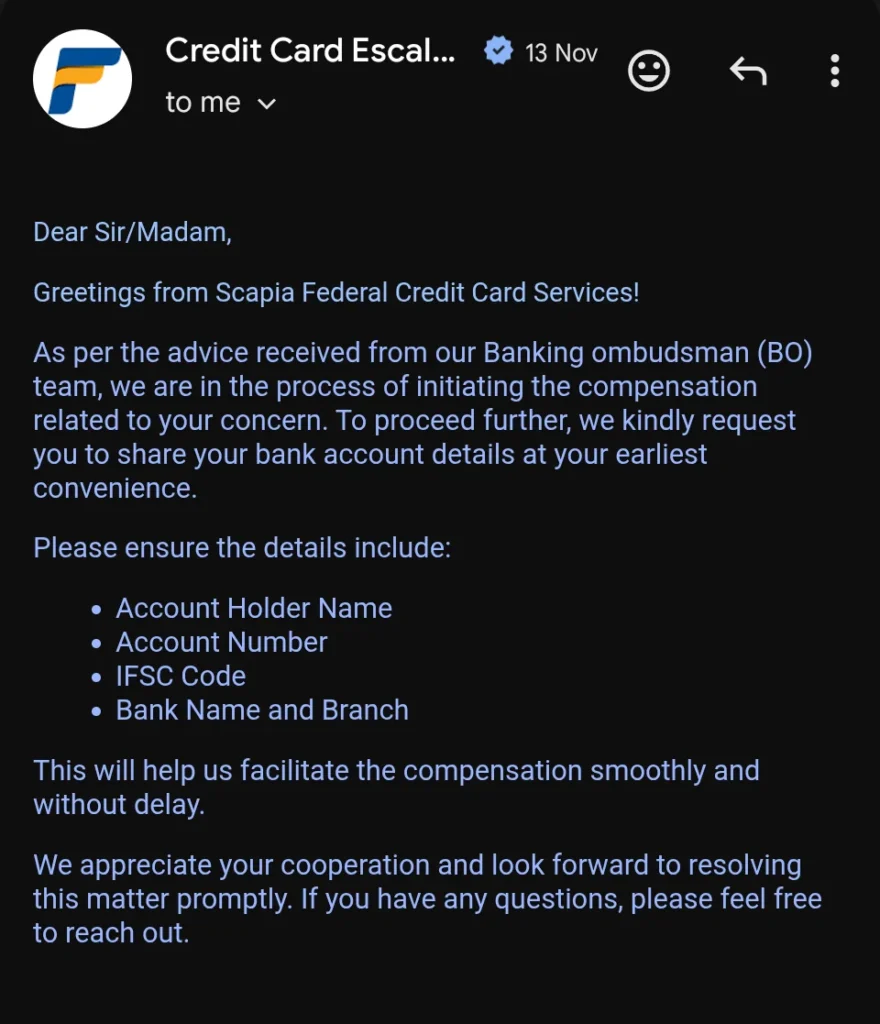

The ₹10,000 Compensation

Under RBI rules, banks are obligated to provide a specific, factual reason for rejection if you demand it.

Recently, one applicant refused to accept Federal Bank’s vague excuse and escalated the issue to the RBI Banking Ombudsman.

The result: After a few months of pressure, the bank’s defense crumbled. They not only approved the Scapia card, but were forced to pay the applicant ₹10,000 in compensation for the wrongful rejection! (Source: Reddit)

This rare victory proves that banks use automated, generic emails as a shield.

So, what are the real reasons they are trying to hide? Let’s look at the actual triggers.

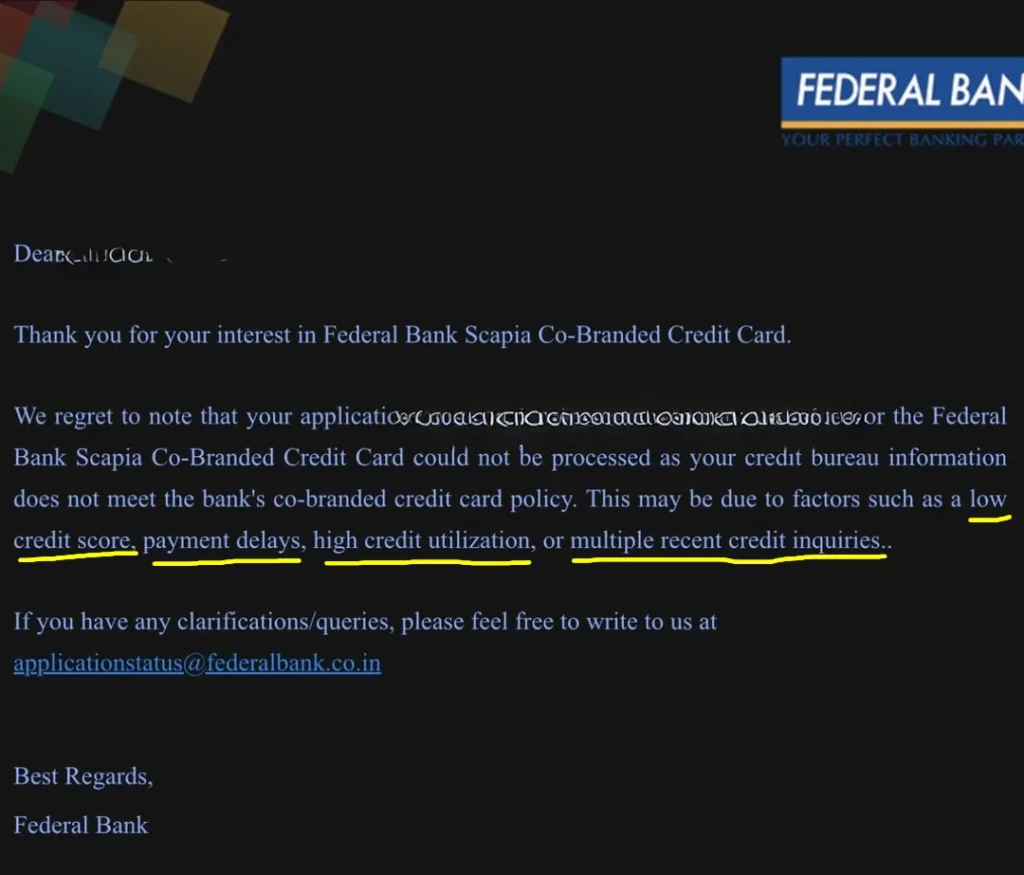

Real Rejection Reasons

When applicants bypass the automated emails and contact the grievance team, the actual rejection triggers emerge.

By analyzing real responses, here is what is really blocking your approval:

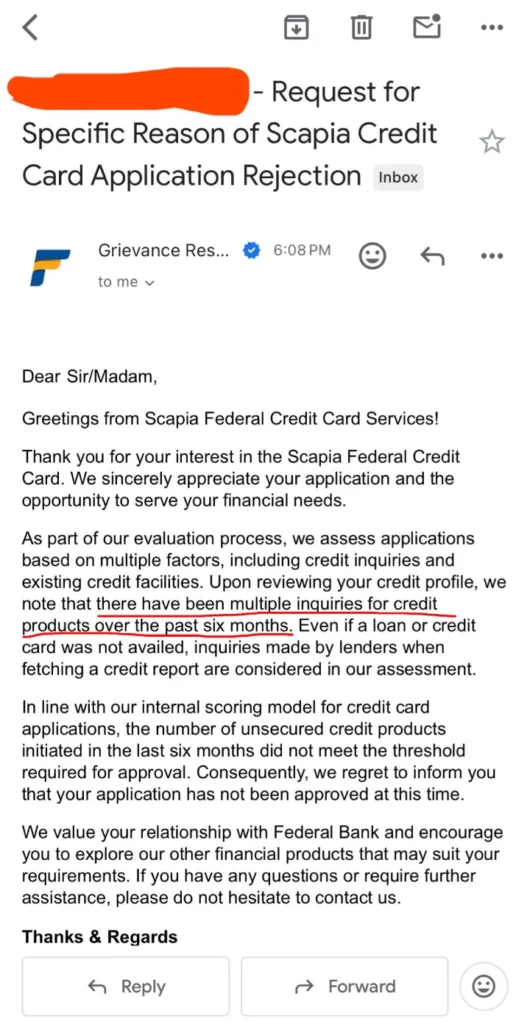

Multiple credit card enquiries

If your CIBIL report shows several recent hard credit inquiries, Scapia’s system automatically flags your profile.

As confirmed by their grievance team, applying for multiple credit cards in a short period leads to an automatic rejection.

A high income or an excellent credit score won’t override this. The automated risk engine views frequent credit applications as a sign of financial instability or “credit hunger”, resulting in an instant denial.

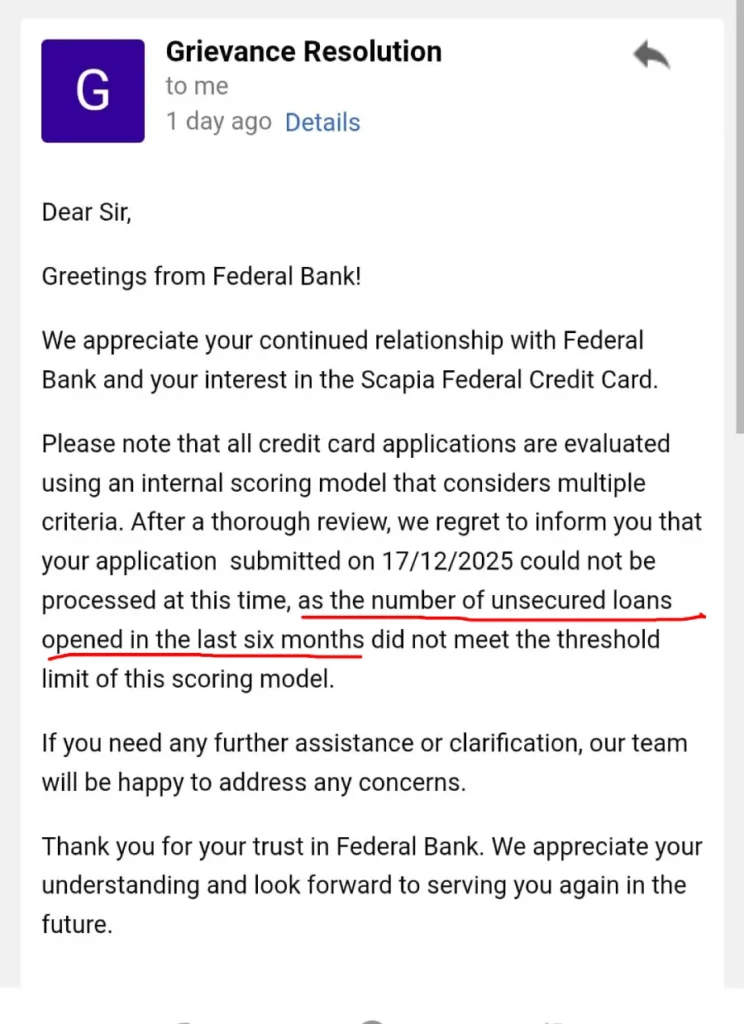

Multiple unsecured loans

No matter if you’re repaying your unsecured loans on time, having multiple active unsecured loans opened recently is a massive red flag for Scapia’s internal risk engine.

As shown in the grievance team’s response, the bank closely monitors the last six months of your credit activity.

If you have recently taken out several personal loans, short-term app loans, or multiple “Buy Now, Pay Later” (BNPL) accounts, the system automatically flags your profile as over-leveraged.

To limit their risk exposure, the automated system rejects the credit card application instantly, regardless of your perfect repayment history.

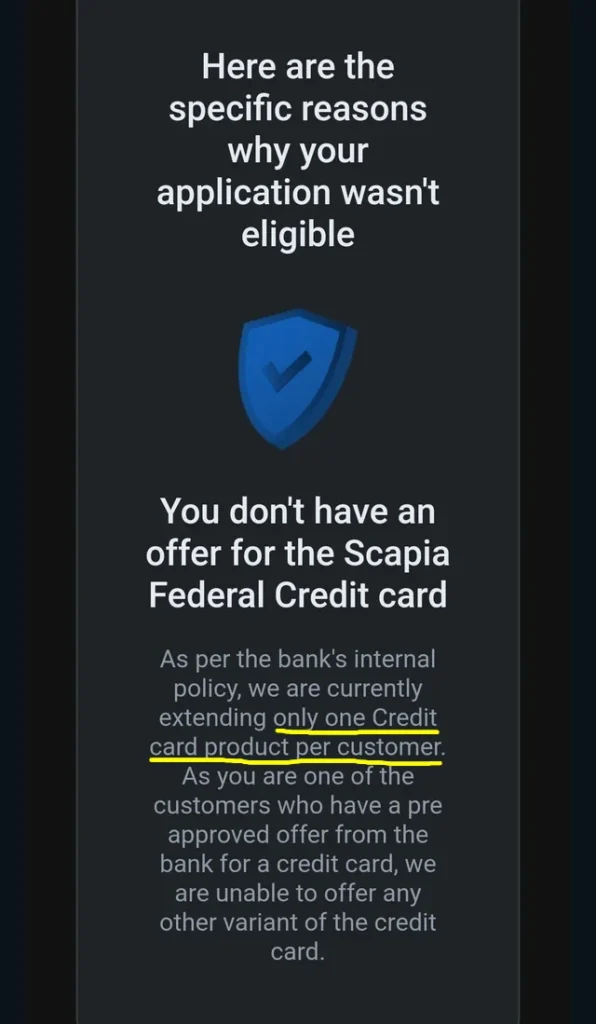

One card per customer rule

Federal Bank enforces a strict “one unsecured credit card per customer” policy.

If you already hold an active Federal Bank credit card (such as the Signet, Celesta, or Imperio), your Scapia application will be automatically rejected. The internal system will not approve a second unsecured credit limit for the same user, regardless of how high your income or CIBIL score is.

Pro-Tip: If you are facing this specific rejection because of an existing Federal Bank relationship, you can bypass this rule by applying for the BOBCARD Scapia variant instead, which operates on Bank of Baroda’s infrastructure.

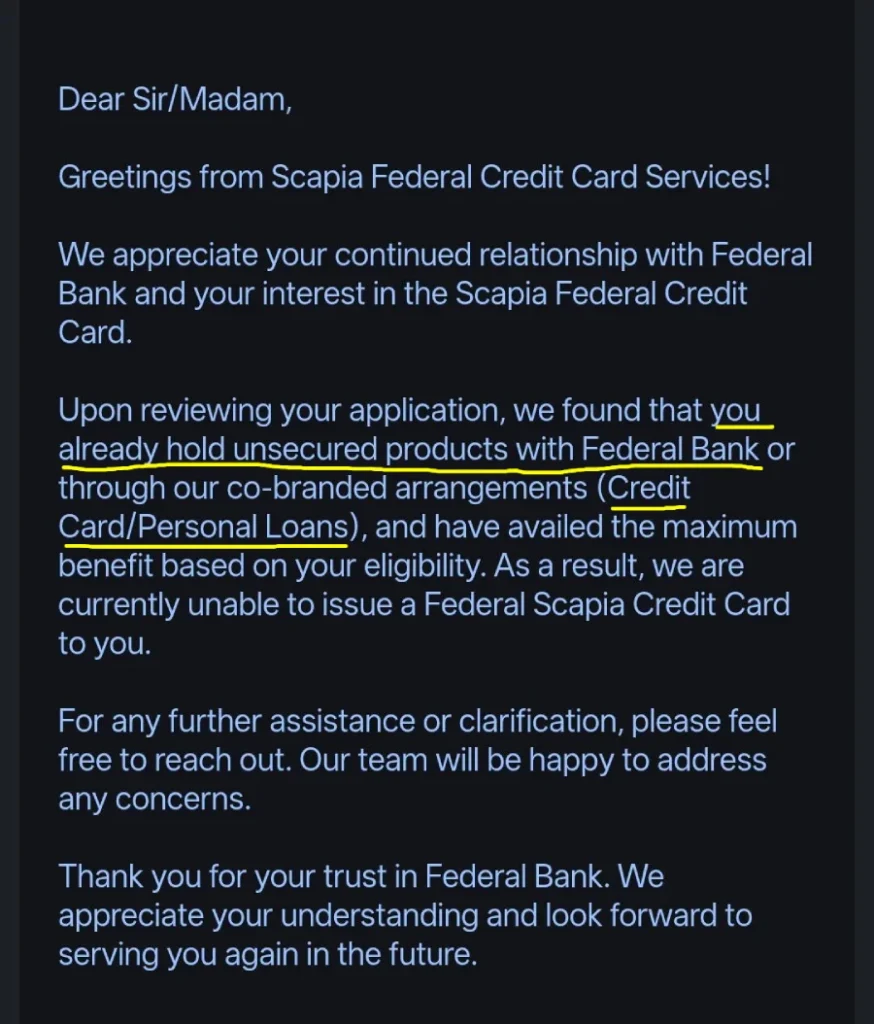

Existing loan with the bank

If you already have an active unsecured loan with Federal Bank, your Scapia credit card application will likely be declined.

Banks strictly cap their risk exposure to individual customers. Even with a flawless repayment record, holding an existing personal loan means the internal system may refuse to extend additional unsecured credit (like a new co-branded credit card) to you until the current loan is closed.

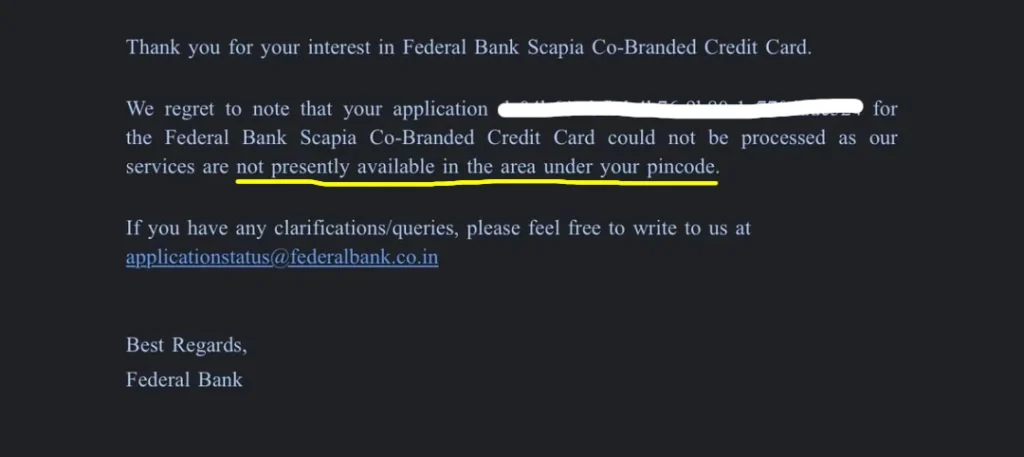

Unserviceable Area

If your residential or office address falls in an unserviceable pin code, your application will be automatically rejected.

Scapia and Federal Bank have a restricted geographical service map. Even with a perfect credit score and high income, the internal system will not approve a card if your registered pin code is not currently serviceable by the bank. This is a hard geographical block, not a reflection of your financial health.

Self-employed aged below 25

If you are self-employed and under 25 years old, the system will automatically reject your application. High income or a great CIBIL score cannot bypass this demographic rule.

If you’re aged below 25, it’s time to look for these best Scapia alternatives.

Other common reasons

Sometimes, the rejection comes down to the fundamental pillars of your credit health.

Even if you clear all the hidden internal filters, the automated risk engine will still reject your application if it detects these basic CIBIL red flags:

- Low credit score: Dropping below the 730-750 mark makes approval for this co-branded card highly unlikely.

- High credit utilization: Consistently using more than 30% of your total existing credit limits flags you as being heavily dependent on credit.

- Late payments: Even a single recent missed payment or default on your CIBIL report acts as an immediate disqualifier.

What to do?

As per Scapia support, you need to wait at least for 90 days before re-applying:

But, you don’t have to wait. Here’s the hack:

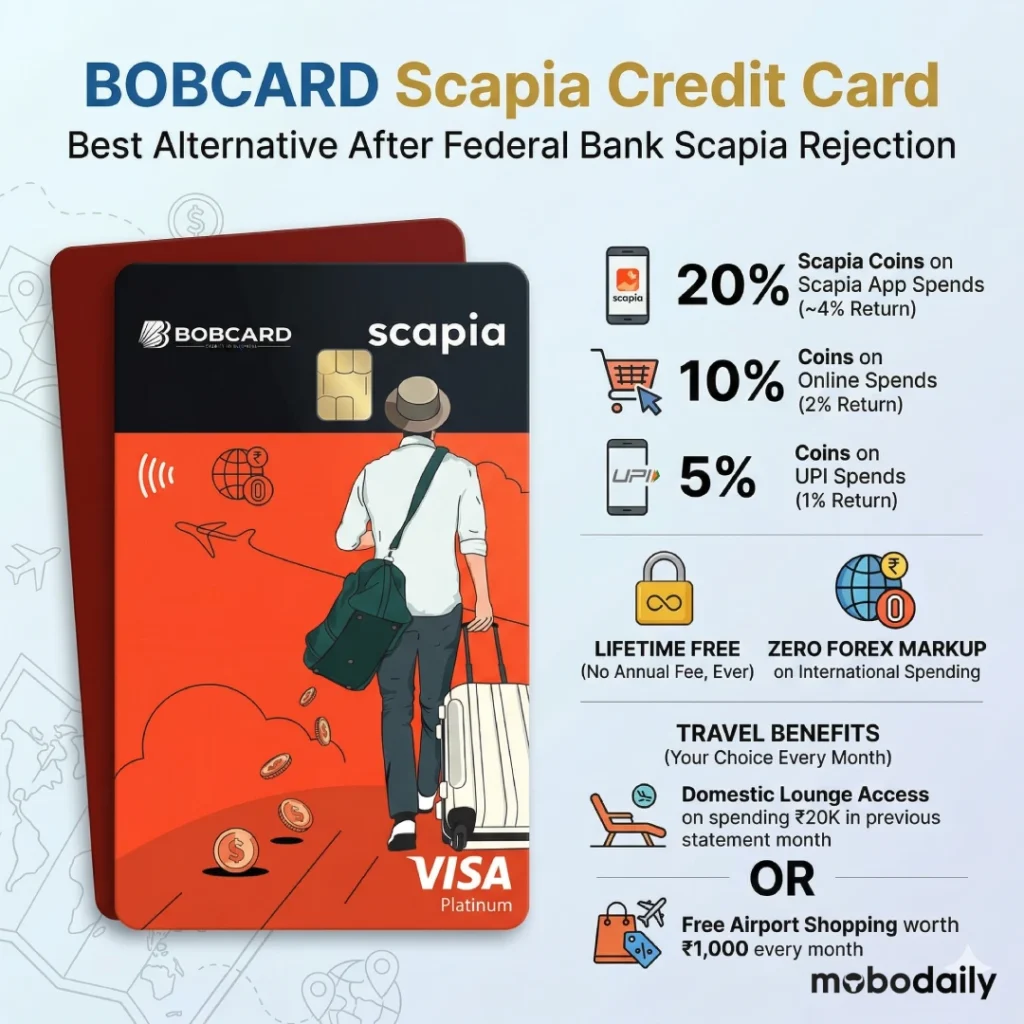

Apply for BOBCARD Scapia

If your credit score and income is good, you can apply for the BOBCARD Scapia variant to bypass the Federal Bank one-card-per-customer policy and other strict parameters.

Many users who got rejected for the Scapia card by the Federal bank, got approved for the BOBCARD Scapia.

However, if your application still gets rejected due to credit health issues, you have to do the 90-day detox to fix your credit card profile.

How to Fix credit score

Here is exactly what you need to do during the 90-day cooling period:

Don’t make credit card enquiry

Every time you hit ‘apply’ for a loan or credit card, a hard inquiry is registered on your CIBIL report. To clear the “credit hungry” tag from Scapia’s system, you need a completely clean slate. Resist the urge to apply for any other credit cards or loans for the next 6 months. Let the old inquiries age out.

Close unsecured loans

If you have active “Buy Now, Pay Later” (BNPL) accounts, short-term app loans, or small personal loans, pay them off and officially close the accounts. Make sure you get a No Objection Certificate (NOC) so they actually reflect as “Closed” on your credit report, freeing up your unsecured limit.

Reduce credit utilization

Start paying off your existing credit card bills before the monthly statement is generated. This ensures the balance reported to CIBIL is very low, keeping your Credit Utilization Ratio (CUR) well below the 30% mark. Scapia’s engine loves applicants who have high credit limits but barely use them.

Rebalance card portfolio

If you hold 10 different credit cards but only actively use 2, consider closing the newly opened, unused ones. A smaller, well-managed portfolio looks much safer to risk algorithms than a massive, cluttered one. However, never close your oldest credit card, as that anchors your overall credit age and stability.

Scapia Devaluation 2026

As shown in the graphic above, getting value from Scapia card is now significantly harder:

- Lounge Access Target Doubled: The monthly spend required to unlock domestic lounge access jumped from a reasonable ₹10,000 to a steep ₹20,000.

- Major Spend Exclusions: You can no longer earn reward on utility bills or insurance payments.

The 2026 Verdict: If you naturally spend ₹20,000+ every month on discretionary categories like dining and shopping, and you strictly want a zero-forex card, Scapia might still work for you.

But if you don’t want a spend condition, check out our curated list of the best credit cards for lounge access with no spend limits to get guaranteed entry without the monthly headache.

Best Scapia Alternatives

Here’s a quick overview on lifetime free Scapia alternatives. For full breakdown, you can read our Complete Guide on Best Scapia Alternatives.

IDFC FIRST WOW

If you want to start building your credit score while still enjoying premium travel perks, the IDFC First WOW is the ultimate starter card.

- Why it’s a great alternative: It offers the exact same 0% forex markup as Scapia. You can travel internationally without worrying about currency conversion fees.

- The LTF Catch: None. It is strictly Lifetime Free with no hidden maintenance charges.

- Who it is for: Students, freelancers, or anyone applying for their very first credit card to build a strong CIBIL history. (Your underlying FD also continues to earn around 6.5% interest!).

BOBCARD Eterna

Normally, cards in this tier charge heavy fees, but BOBCARD is currently running a massive promotional campaign making the Eterna Lifetime Free for eligible applicants.

- Why it’s a great alternative: It offers truly unlimited domestic lounge access (subject to quarterly spends) and a massive 3.75% reward rate on dining, travel, and international spends. Even with a 2% forex fee, its high reward rate mathematically beats Scapia’s 0% forex offer.

- The LTF Catch: This is a limited-time promotional offer (currently valid until March 2026). You must also meet their strict eligibility criteria: an income of over ₹12 Lakhs per annum.

- Who it is for: High-earning individuals who want top-tier premium benefits without paying a ₹2,499 annual fee.

AU ixigo

If you are a hardcore traveler looking for zero forex markup, lounge benefits, and direct flight/hotel discounts, this is currently the best card in the Indian market.

- Why it’s a great alternative: It completely outclasses Scapia by offering 0% forex markup, domestic and railway lounge access, and international lounge access. You also get a flat 10% discount on flights and hotels booked via the ixigo app.

- The LTF Catch: This card is only Lifetime Free if you are a new AU Bank credit card customer applying during their promotional period.

- Who it is for: The frequent domestic and international traveler who wants maximum travel utility from a single card.

Considering AU Ixigo as a Scapia alternative? Read our detailed comparison: Scapia vs AU Ixigo — Which Card Should You Get?

Niyo Global Secured

Niyo is a massive favorite among the backpacking and student communities, offering a seamless, tech-first travel ecosystem.

- Why it’s a great alternative: Like Scapia, it offers a true 0% forex markup using live exchange rates. Plus, you actually get International Lounge Access (via the Niyo Lounge Pass) if you meet their international spend criteria—something Scapia doesn’t offer at all.

- Who it is for: Travelers who want a flawless mobile app experience for managing international trips, booking visas, and tracking expenses without needing an existing credit score.

Uni Gold X

If you travel occasionally but spend a lot of money online, the Uni Gold X is an incredibly unique and rewarding alternative.

- Why it’s a great alternative: It offers the coveted 0% forex markup for your travels, but its real superpower is its rewards system. You get 5% to 8% Gold-Back on purchasing top brand vouchers (Amazon, Myntra, Zomato) and 7% Gold-Back on flights via the Uni Store.

- The Trade-off: You do not get airport lounge access with this card.

- Who it is for: The traveler cum online shopper. Because your cashback is awarded in 24K Digital Gold, the value of your rewards actually goes up when gold prices rise!

However, SBI Cashback is my go to card. Checkout the SBI Cashback Card Review & Hacks to get 5% cashback on utility and fuel spends!

Credit Card Eligibility Checker

Note: This eligibility checker is for informational purposes only. While it estimates your eligibility based on standard bank criteria, final approval and credit limits are strictly determined by the issuing bank upon a full credit check.

Bottom Line

Getting hit with a Scapia card rejection stings, especially when the reasoning feels automated and unfair. But as we've seen, the 2026 devaluations mean you might actually be dodging a bullet.

Don't let a Federal Bank algorithm dictate your travel plans. Whether you choose the guaranteed approval of the IDFC WOW, the premium perks of the AU ixigo, or the appreciating gold-back of the Uni Gold X, there is a better card out there waiting for your approval.

Pick the alternative that fits your profile, apply today, and get back to planning your next trip!

Contact us to get free gift vouchers 💸 when you apply cards recommended by us.

FAQs

Why did Federal Bank reject my Scapia card application despite a good CIBIL score?

Federal Bank uses a very strict internal risk algorithm that goes beyond just your CIBIL score. The most common reasons for rejection include having more than 5 hard credit inquiries in the last 6 months, living in an "unserviceable" pin code, or already holding an active Federal Bank credit card (like the OneCard or Jupiter Edge).

How long should I wait before reapplying for the Scapia card?

Scapia support officially advises waiting at least 90 days before reapplying. However, for the best chance of approval — especially if your rejection was due to multiple enquiries or an unsecured loan — waiting 6 months (180 days) is ideal. Use that time to reduce credit utilisation below 30% and avoid new credit applications.

Does a Scapia credit card rejection lower my CIBIL score?

The rejection itself does not lower your score. However, when you apply, Federal Bank initiates a "hard inquiry" to check your credit report. This hard inquiry typically causes a temporary dip of 2 to 5 points in your CIBIL score. If you spam applications, these inquiries pile up and can damage your score significantly.

Can I get the Scapia card if I already have a Federal Bank credit card?

Currently, No. Federal Bank enforces a strict "One Bank, One Card" policy. If you already hold a Federal Bank signet card, OneCard, or any other co-branded Federal card, your Scapia application will be automatically rejected. Pro-tip: You can try applying for the BOBCARD Scapia variant to bypass this specific rule.

Is the Scapia card still Lifetime Free (LTF) in 2026?

Yes, the Scapia card is still issued as Lifetime Free with no joining or annual fees. However, following the 2026 devaluations, the cost to unlock its main benefit—domestic lounge access—has doubled, requiring you to spend ₹20,000 every billing cycle.

Which is the best alternative to the Scapia card right now?

If you want zero forex markup and travel benefits, the AU ixigo Credit Card is the best direct replacement. If you have a low credit score or want guaranteed approval, the FD-backed IDFC FIRST WOW is your best bet. If you want a zero forex card that also rewards your daily UPI spends with appreciating assets, go for the Uni Gold X.

Disclaimer: The information provided in this article, including credit score improvement tips and RBI Banking Ombudsman case studies, is for educational and informational purposes only. Individual results, bank approvals, and compensation claims vary strictly by case. I am not a financial advisor, and acting on this information is at your own risk. Mobodaily is reader-supported. We may earn a small commission if you apply for a credit card through the links in this article. This does not affect our editorial independence. Read our full privacy policy and disclaimer.

- Axis Horizon Credit Card Review: Worth ₹3,540 Fee? - July 29, 2026

- HDFC Marriott Bonvoy Credit Card Review (2026) - July 29, 2026

- HDFC Tata Neu Infinity Credit Card Review 2026 - July 24, 2026