Is HDFC Millennia worth applying in 2026?

I upgraded to the HDFC Millennia Credit Card from my lifetime-free HDFC Moneyback card back in 2022, and four years later, it’s still active in my wallet alongside my Swiggy OG, Tata Neu Infinity, and Marriott Bonvoy.

That alone should tell you something — but let’s get into the actual numbers, terms, and experience so you can decide if it deserves a spot in yours.

Overview

| Card Type | Cashback |

| Network | Visa / Mastercard / RuPay |

| Cashback Rate | Up to 5% |

| Annual Fee | ₹1,000 + GST |

| Best For | 5% back on online shopping |

🔒 Safe & Secure via HDFC Bank

Eligibility

| Criteria | Salaried | Self-Employed |

|---|---|---|

| Age | 21–40 years | 21–40 years |

| Income | Above ₹35,000/month | ITR above ₹6 lakh/year |

| Suggested CIBIL Score | 750+ | 750+ |

| Nationality | Resident Indian (NRE accepted) | Resident Indian (NRE accepted) |

HDFC doesn’t publish a hard CIBIL cutoff — the 750+ benchmark above is the commonly observed threshold for approval, not an officially guaranteed number.

Having an existing HDFC salary or savings account can also improve your approval odds even if your income is borderline.

Annual Fee

This isn’t a free card, but the fee is easy to avoid in practice:

| Joining Fee | ₹1,000 + GST |

| Welcome Benefit | 1,000 CashPoints |

| Renewal Fee | ₹1,000 + GST |

| Renewal Benefit | – |

| Fee Waiver | ₹1L annual spend |

In four years, I’ve never actually paid this fee — ₹1 lakh in annual spend is a low bar if you’re using this as a primary card for online shopping.

SBI Cashback Card

The OG cashback card for regular online shoppers.

- 5% cashback on all online spends 🛒

- No merchant restrictions

Earning CashPoints

| Category | Cashback Rate | Monthly Cap |

|---|---|---|

| Partner brands | 5% | 1,000 CashPoints/month |

| All other eligible spends | 1% | 1,000 CashPoints/month |

Partner brands: Amazon, Flipkart, Myntra, Tata CLiQ, BookMyShow, Cult.fit, Sony LIV, Swiggy, Zomato, and Uber (travel/commute only).

Other eligible spends include wallet/prepaid/gift card loads, and direct education payments too. This is a rare scenario among entry-level cards.

Excluded spends: Fuel, all EMI transactions (Smart EMI/Dial-a-EMI, even preclosed), rent, government payments, cash advances, card fees, education payments via third-party apps (CRED, PayTM, etc.)

Redeeming CashPoints

| Best Redemption Method | Statement credit |

| Redemption Rate | 1 CashPoint = ₹1 |

| Min Redemption | 500 CashPoints |

| Max Redemption | 3,000 CashPoints per month |

| Redemption Fee | ₹50 + GST |

| Points Validity | 2 years |

| Other Options | Flights/Hotels via SmartBuy, Rewards catalogue (1 CP = ₹0.30) |

Other redemption options include flights/hotels via SmartBuy, and rewards catalogue but they offer poor value at 1 CP = ₹0.30.

💡 Tip: Accumulate points up to the 3,000 monthly cap to minimize the impact of the fee. Since the ₹50+GST redemption fee is fixed, avoid frequent, small redemptions, which can erode your effective cash back.

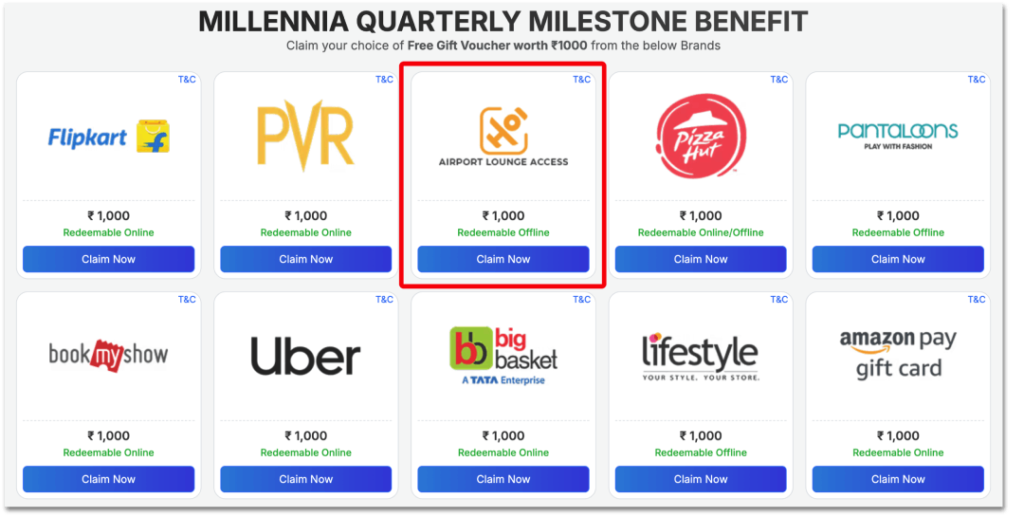

Milestone Benefit / Lounge Access

Unlock a quarterly milestone voucher by spending ₹1,00,000 or more in a calendar quarter.

Upon qualification, you can choose between a lounge access voucher or a ₹1,000 brand voucher.

💡 Takeaway: Since direct lounge access is no longer a standard feature, I recommend opting for the ₹1,000 brand voucher. Use other cards for airport lounge access — no spend.

Scapia Card

Best beginner travel card with lounge access and zero forex markup.

- Unlimited lounge access

- Zero forex markup

- Zero annual fee

Why I Hold HDFC Millennia

I switched from the lifetime-free Moneyback card in 2022. The decision was simple: the Millennia’s math favored my spending habits. The ₹1,000 monthly cashback potential and quarterly milestones made the annual fee a non-issue from day one.

Currently, I route approximately ₹20,000/month through partner merchants to maximize the 5% cap. For instance, on a recent phone purchase, bank discounts combined with cashback brought my real cost down by nearly ₹4,000.

This card works as part of a strategic HDFC “quad-core” setup in my wallet:

- Millennia: 5% cashback on partner shopping.

- HDFC Swiggy: Dining and food delivery.

- Tata Neu Infinity: Tata brands and UPI payments.

- Marriott Bonvoy: Annual free nights and lounge access.

My only gripe? My credit limit has been stagnant for 18 months with no clear path to an upgrade. However, the card’s core value has remained remarkably consistent.

Mobodaily Rating

| Factor | Rating |

|---|---|

| Fee Value | 4.5/5 |

| Cashback Value | 4.3/5 |

| Redemption Flexibility | 3.5/5 |

| Customer Service | 4.5/5 |

| Overall | ⭐️ 4.2/5 |

Final Verdict — Should You Apply?

Yes, the HDFC Millennia deserves a slot in your wallet in 2026.

With 5% back on partner brands, it offers 1% back on “ignored” categories like direct education payments, insurance premiums, and wallet/gift card loads that most entry-level and mid-premium cards exclude from rewards.

If your spends are high, you can stack it with Tata Neu Infinity — using Millennia for partner offers and broad online spends, while routing Tata, UPI, and travel-heavy spends to Tata Neu to squeeze extra value out of the same monthly budget.

🔒 Safe & Secure via HDFC Bank

Disclaimer: This review is for informational purposes only and not financial advice. Bank terms and eligibility criteria change; please verify details on the official HDFC Bank website before applying. This review contains affiliate links. If you use them, we may earn a small commission at no extra cost to you.

- Get Up to ₹750 Free Voucher with Visa Credit Cards - July 14, 2026

- HDFC Millennia Credit Card Review 2026 - July 14, 2026

- Axis My Zone Vs Axis Rewards Credit Card 2026 - June 27, 2026